The Australian Governance Masters Index Fund (AQF.AX) is a listed investment scam run by the fraudsters from Dixon Advisory & Superannuation Services. With revolting hypocrisy, AQF ostensibly invests in the "best governed" ASX100 companies, aiming to hold between 75-85% of the index. This zeal for governance does not extend to the company itself. AQF is run by criminals that deliberately manipulate the company's illiquid shares. With ASIC's tacit approval, AQF sets its own share price at higher than asset backing, partly by performing buybacks.

This fixed "market" price is of course only sustainable if AQF's granny investors do not actually try to sell at the fake price. In case of sustained net investor outflows, the company could at most support its share price at actual NTA (which is of course post-tax, whatever the criminals may profess to "believe"). AQF also issues shares to investors while making the fraudulent representation that it trades at a "market" price, whereas in reality AQF sets its own price. There is currently one buyer and one seller for AQF, namely AQF itself.

AQF does not even disclose actual NTA in its weekly disclosure documents, instead only reporting "pre-tax" NTA (i.e. an imaginary NTA if taxes were abolished). The criminals then set the share price floor at this inflated figure. Currently, AQF's "pre-tax" NTA is $1.90, with its actual NTA estimated at several percent less.

http://www.asx.com.au/asxpdf/20131030/pdf/42kfv3p1mhhpl1.pdf

That ASIC allows AQF to openly ramp its share price above its asset backing is an absolute disgrace, proof positive that the regulator is completely ineffectual against even the most blatant fraud. If criminal directors just claim to "believe" they are acting for the good of shareholders, and fill out the forms, they are allowed to openly run a ponzi scheme.

Thursday 31 October 2013

Wednesday 30 October 2013

Argo Investments intentionally falsifies its NTA

Argo Investments (ARG.AX) has repeatedly committed securities fraud by reporting inflated NTA and claiming that its shares trade at a discount to NTA. ARG has admitted to making such representations to financial advisers, deceiving clients into feeding money into a scheme actually priced at a significant premium to NTA. ARG currently inflates its reported NTA by 14% by using "pre-tax" estimates, based on the "opinion" that they can exclude taxes due on unrealized capital gains, yet still include the full effect of the gains themselves, effectively reporting a hypothetical NTA in a world where taxes have been abolished.

But this is not a matter of opinion. Even if criminals are of the "opinion" that one plus one equals three, that does not them the right to use such maths in their books. This is fraud, regardless of the criminals' "opinion". Net means net, i.e. after costs such as tax, regardless of what the fraudsters opine. The value of something is what you can sell it for, not what you can sell it for assuming there were no such thing as taxes. ARG goes one step further than other criminal LICs by not even including the words "pre-tax" in their NTA disclosure documents, which is blatantly illegal, as it gives the impression they are disclosing their actual NTA when they are not. ASIC does nothing about this deliberate recurring misrepresentation.

http://www.asx.com.au/asxpdf/20131004/pdf/42jv87rm1wpjqb.pdf

ASIC could just mandate that funds have to report their actual NTA and are forbidden to use deliberately deceptive metrics such as "pre-tax NTA", with or without "explanatory" footnotes. But ASIC is completely useless, and makes no attempt at ensuring disclosure is accurate or presents a fair view, merely being concerned with quantity and encouraging frequent fraudulent disclosure. Australian investors can't even expect something as fundamental as an accurate and unskewed view of the value of a fund's assets in disclosure documents. Instead investors are given director's "opinions" of what the criminals think the assets should be valued at.

The idea that net assets can ignore taxes is ludicrous, it has absolutely no basis in reality. Neither does it make any sense to doublecount upcoming dividends as a receivable in net assets. But since criminals are freely allowed to define their own reality in Australia, anything goes. Over the last year more and more funds have been purposefully ramped above NTA, so that a fraudulent profit from subsequent share issuing to scammed granny investors can be achieved.

But this is not a matter of opinion. Even if criminals are of the "opinion" that one plus one equals three, that does not them the right to use such maths in their books. This is fraud, regardless of the criminals' "opinion". Net means net, i.e. after costs such as tax, regardless of what the fraudsters opine. The value of something is what you can sell it for, not what you can sell it for assuming there were no such thing as taxes. ARG goes one step further than other criminal LICs by not even including the words "pre-tax" in their NTA disclosure documents, which is blatantly illegal, as it gives the impression they are disclosing their actual NTA when they are not. ASIC does nothing about this deliberate recurring misrepresentation.

http://www.asx.com.au/asxpdf/20131004/pdf/42jv87rm1wpjqb.pdf

ASIC could just mandate that funds have to report their actual NTA and are forbidden to use deliberately deceptive metrics such as "pre-tax NTA", with or without "explanatory" footnotes. But ASIC is completely useless, and makes no attempt at ensuring disclosure is accurate or presents a fair view, merely being concerned with quantity and encouraging frequent fraudulent disclosure. Australian investors can't even expect something as fundamental as an accurate and unskewed view of the value of a fund's assets in disclosure documents. Instead investors are given director's "opinions" of what the criminals think the assets should be valued at.

The idea that net assets can ignore taxes is ludicrous, it has absolutely no basis in reality. Neither does it make any sense to doublecount upcoming dividends as a receivable in net assets. But since criminals are freely allowed to define their own reality in Australia, anything goes. Over the last year more and more funds have been purposefully ramped above NTA, so that a fraudulent profit from subsequent share issuing to scammed granny investors can be achieved.

Tuesday 29 October 2013

Throwing caution to the wind

ASF Group (AFA.AX) describes itself as involved in the "identification, incubation and realisation of embryonic opportunities", claiming business activities in the fields of tourism, commodities trading, property, travel, energy, resources, investments and financial services, and as a "creator and facilitator of two-way cross-border investments, trade and technology transfers". In reality, AFA is simply another fraudulent listed investment company. In its bizarre FY13 annual report, AFA reported a loss of $30.5m based on revenues of $1.7m. Net assets amounted to $1.2m, down from $29.2m in FY12. The "market" still mysteriously values AFA at $56m.

A year ago, AFA was touted by the Sydney Morning Herald small cap shill, in an Under The Radar column straight out of The Onion. The shill admitted to having no idea how the company purportedly made money. The slimy shill then recommended small investors "throwing caution to the wind - rather than digging too deeply into the detail." The small cap shill then praised how AFA's chairman once "won a singing contest" and lauded AFA for having "very few costs".

A year ago, AFA was touted by the Sydney Morning Herald small cap shill, in an Under The Radar column straight out of The Onion. The shill admitted to having no idea how the company purportedly made money. The slimy shill then recommended small investors "throwing caution to the wind - rather than digging too deeply into the detail." The small cap shill then praised how AFA's chairman once "won a singing contest" and lauded AFA for having "very few costs".

http://www.smh.com.au/business/under-the-radar/a-small-cap-in-the-dragons-saddle-20120829-24zoq.html

How much the shill was bribed for this insane column, if anything, is of course unclear. Lacking the slightest shred of integrity, it stands to reason the shill would sell himself for next to nothing. If he wasn't bribed for this column, in some ways that makes his conduct even more pathetic.

AFA engages in ramping, revaluation and reclassification of assets, as well as various related party transactions and loans. AFA has never had actual positive cash flows, it solely functions as a vehicle for securities fraud. With ASIC's blessing, AFA simultaneously issues and buys back its shares, allowing it to control its own "market" price. According to ASIC, such manipulation is just a great feature of the "market".

How much the shill was bribed for this insane column, if anything, is of course unclear. Lacking the slightest shred of integrity, it stands to reason the shill would sell himself for next to nothing. If he wasn't bribed for this column, in some ways that makes his conduct even more pathetic.

AFA engages in ramping, revaluation and reclassification of assets, as well as various related party transactions and loans. AFA has never had actual positive cash flows, it solely functions as a vehicle for securities fraud. With ASIC's blessing, AFA simultaneously issues and buys back its shares, allowing it to control its own "market" price. According to ASIC, such manipulation is just a great feature of the "market".

Monday 28 October 2013

Just shilling and enjoying the ride

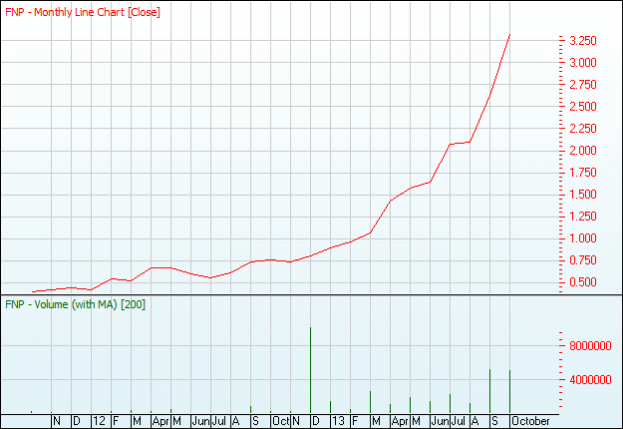

It is standard business practice for Australian investment companies to ramp the share prices of controlled holdings, with the fraudulent "market prices" giving rise to unrealized profits. Ramped assets are packaged in asset backed securities and dumped on granny investors as companies issue shares. The result is long term shareholder value destruction, interspersed with temporary ramps to benefit insiders. Associated shills play a key part in this securities fraud, with the Sydney Morning Herald even having a dedicated column for shilling ramped small caps. The Under The Radar column features a particularly vile individual shilling stocks he is perfectly aware are manipulated, with his latest column advocating the exponentially ramped FNP.

The column touting FNP makes for surreal reading.

The shill freely admits that the recent exponential ramp of FNP "defies logic". He acknowledges that FNP is trading at 205 times its FY13 net profit before abnormals. The shill is aware that a single shareholder holds 60% of FNP, that the top twenty shareholders own 90% of common shares and 98% of convertibles. The shill claims to "not understand" why the "market" suddenly values FNP at half a billion dollars. Yet this is apparently of no concern. The shill recommends granny investors keep holding this manipulated stock and just "enjoy the ride".

Of course, were the shill to admit that FNP is ramped, he would be confessing to being an accomplice to securities fraud. So lo and behold, the shill feigns complete innocence. The Under The Radar shill has ties to criminal listed investment companies and has repeatedly aided them in securities fraud. MIR holds a major stake in FNP, and may have been the source for the shill's anonymous quotes in the article. The shill also recommended investors "enjoy the ride" when CTN ramped BCC.

For reference, here is the ride that the shill thinks investors are "enjoying" at BCC, showing the now familiar pattern of long term shareholder value destruction interspersed with ramps to benefit insiders:

When one day the shill shuffles off this mortal coil, leaving the world an unequivocally better place, hopefully he will enjoy his well-deserved ride straight to hell.

Friday 25 October 2013

Taxing times in Bermuda

As part of its zero enforcement policy, ASIC takes no action against companies engaging in share manipulation and sham transactions, as long as the proper forms are filled out. Not only can listed investment companies avoid tax through correctly structured international sham transactions and "loans" between related parties, they can actually claim a tax benefit. As a recent example, ZER and Utilico Investments engaged in a series of related party transactions, write-offs and loans, resulting in an annual report that best can be described as comical.

Domiciled and tax-exempt in the Bermudas, ZER was listed on the ASX in June 2013 and recently submitted its FY13 annual report, reporting an immediate loss of $9,338,686 and a tax benefit of $546,439 from the R&D tax offset.

http://www.asx.com.au/asxpdf/20131018/pdf/42k3xct105hptw.pdf

ZER had revenues of $310,000 from interest and foreign currency gains in FY13, with expenses and write-offs totaling $9,615,996. The company also took out a "loan" of $4,577,000 from Utilico Investments, resulting in current liabilities twice that of current assets. Nevertheless, KPMG in South Africa signed off on the annual report unreservedly. This mysterious business plan apparently appeals to investors, as the "market price" of ZER has risen 20% since listing. Of course, this may have been helped by the fact that the top twenty shareholders own 95.26% of the company, with the aforementioned Utilico Investments holding a 77.35% stake. No matter. According to ASIC, ZER trades at a market price and belongs on the ASX with its brethren fraudulent investment companies.

Domiciled and tax-exempt in the Bermudas, ZER was listed on the ASX in June 2013 and recently submitted its FY13 annual report, reporting an immediate loss of $9,338,686 and a tax benefit of $546,439 from the R&D tax offset.

http://www.asx.com.au/asxpdf/20131018/pdf/42k3xct105hptw.pdf

ZER had revenues of $310,000 from interest and foreign currency gains in FY13, with expenses and write-offs totaling $9,615,996. The company also took out a "loan" of $4,577,000 from Utilico Investments, resulting in current liabilities twice that of current assets. Nevertheless, KPMG in South Africa signed off on the annual report unreservedly. This mysterious business plan apparently appeals to investors, as the "market price" of ZER has risen 20% since listing. Of course, this may have been helped by the fact that the top twenty shareholders own 95.26% of the company, with the aforementioned Utilico Investments holding a 77.35% stake. No matter. According to ASIC, ZER trades at a market price and belongs on the ASX with its brethren fraudulent investment companies.

The charade: A guide to answering ASX price queries

Australian regulators have a zero enforcement policy regarding share price manipulation, with ASIC never intervening against share price ramps. The only consequence for companies deliberately ramping their share price is a potential ASX price query, a form letter asking if the company is aware of any undisclosed information that could explain recent price movements. Every single time this occurs, the company in question then replies that it has no idea whatsoever what could have caused the price movement. And that's it. Since all replies to ASX queries are essentially identical, the whole exercise is just a charade, with absolutely no point. Included below is a standard response that ASX instead could complete and send to itself. This would save everyone time and have the same (non-existent) benefit as the current charade.

http://www.asx.com.au/asxpdf/20131004/pdf/42jtqrs5vk2y3j.pdf

Next time, Elvis could just fill out the standard response and send it to himself, with identical end result.

Dear ASX,

Thank you for your letter dated [insert date] regarding a change in volume and price of shares in [insert company name]. In reply to your questions:

1. The company is not aware of any information concerning it that has not been announced, which if known could be an explanation for recent trading in the company's securities.

2. Not applicable.

3. No.

4. The company confirms it is in compliance with the listing rules and in particular with listing rule 3.1.

Yours faithfully, [insert name].This form letter could be used by ASX in every instance. MNW provides a nice example of how this works. Ramped 1000% in three months, MNW issued shares and options starting at $0.10 to accomplices. These accomplices then ramped the share price above $0.40. The management of MNW not only knew the reason for the ramp, but had engineered it themselves, yet when queried by ASX supplied the following response:

http://www.asx.com.au/asxpdf/20131004/pdf/42jtqrs5vk2y3j.pdf

Next time, Elvis could just fill out the standard response and send it to himself, with identical end result.

Subscribe to:

Posts (Atom)